UMG Investment Thesis

UMG offers the oportunity to own the #1 player in a global oligopoly, benefitting from secular growth with high margin royalty revenues and compounding FCF generation at a discounted valuation.

Investment Summary

Universal Music Group (UMG) is the dominant player in a global, stable oligopoly with decades-long secular growth of global music consumption with high margin, defensible, predictable royalty revenues, a long runway of +DD% earnings and FCF generation, with an underutilised balance sheet and low capital markets dependency.

I believe UMG is currently mispriced, with a 25% discount to NFLX which implies the market is ascribing a premium to eyeballs over ears.

A material rerating is due, likely to be triggered by DSP (digital service provider) price increases, accelerated paid subscription penetration and best in class margin expansion.

Industry Overview

The Recorded Music industry is worth $31bn and is forecast to grow at a +8% CAGR over the next decade, driven by secular themes of the shift to streaming, improving monetisation towards that of the Video industry, and new opportunities such as Generative AI and new listening occasions.

A quick primer on the music industry -

Every song has 2 copyrights:

1) the master recording - this is owned by record labels which represent artists. The labels generate royalties from the master recording every time that song is played on the radio, streamed on Digital Service Provider platforms (DSPs), performed or used in films/ TVs/ video games/ other media.

2) the musical composition & lyrics - this is owned by music publishers which represent songwriters and get compositions recorded by Record Labels.

Once there is a recording, the publisher and songwriter share the royalties generated. Labels share 15-25% of revenue with the artists and songwriters.

The industry is a stable oligopoly between 3 record labels (“majors”): UMG, Sony Music Entertainment (SME) and Warner Music Group (WMG). Content is concentrated with the 3 majors representing 70% industry revenue. DSPs need content from all 3 majors to offer a competitively viable offering which results in the labels essentially having a monopoly on each of their artists.

Business Overview

UMG is the leading major label globally in the music industry with segments as follows:

Recorded Music (77% revenues, 23% margin)

Music Publishing (18% revenues, 22% margin)

Merchandising (5% revenues, 7% margin): sale of merchandise from touring, physical retail and eCommerce.

UMG is the largest music company globally with the best roster of artists and catalogue (songs older than 3 years):

#1 in Recorded Music with 32% market share (#2: SME at 21%, #3: WMG at 16%)

#2 in Music Publishing with 23% market share (#1: SME at 25%, #3: WMG at 11%)

80% market share based on publishing rights, earning UMG best in class negotiating power

9 of the top 10 global recording artists in 2023 (source: UMG FY2023 results presentation)

6 of the top 10 global artists on Spotify, 13 of the top 20 global songs on Apple Music, 3 of the top 5 global songs on Youtube (source: UMG FY2023 results presentation)

80% of UMG’s revenues are a predictable, recurring and scalable annuity (subscriptions & streaming, licensing and music publishing).

Scale is key in expanding intellectual property. UMG generates 30%/ 60% more revenues than SME/ WMG, which earns UMG more firepower to spend on Artists & Repertoire (like R&D) and catalogue investments.

Catalogue makes up 60% revenue and 75% EBIT, meaning UMG is less dependent on new hits compared to the Video industry. Existing catalogue songs have low marketing requirements, making it a high margin and stable royalty stream.

UMG has a world class management team with deep industry experience - CEO Sir Lucian Grainge has spent his entire career in the music industry and is widely recognised as the industry’s most important executive, having navigated the industry’s pivot from existential threat from piracy towards music streaming and renewed, higher quality growth.

UMG uses FCF to acquire catalogue assets, pay a 2.5% dividend yield and could in the future return capital via buybacks. UMG runs a strong balance sheet with 1x leverage, versus 3x for WMG, which affords it greater flexibility to invest in artists, catalogues and new markets. This makes UMG better able to drive further growth and defend its moat.

Thesis & Differentiated View

1. High growth with +8% revenue CAGR outlook…

Music is undermonetised, and I expect a new cycle of recurring price increases Music is the lowest-cost but highest-value forms of entertainment given it can be consumed at any hour as a primary activity or secondary activity. The charts below show that 1 hour of music streaming costs fractions of an hour of other entertainment.

I expect regular price increases in the music streaming industry as they already are in the SVOD industry (Netflix has raised pricing by +80% over the last decade), whereby price increases directly benefit UMG’s subscription revenue growth rate. All major DSPs have increased prices by at least 10% in the past 2 years (Spotify: +15% as of April 2024, Apple Music +40% as of October 2022, Amazon Music +13% as of February 2023, Youtube +17% as of July 2023). Assuming this continues, I expect this to translate to organic sales growth contribution of ~+120-150 bps p.a.

I think the Music Streaming industry has lagged the price increases of the SVOD industry due to content costs; the SVOD platforms invest in production development which drives up the cost of the service, necessitating higher subscription fees. The cost for a music streaming platform to license music from a label is not as onerous however.

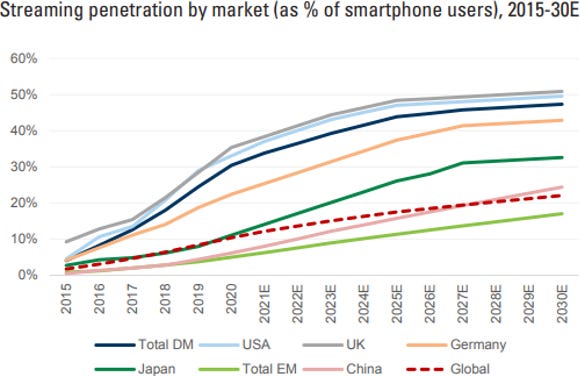

Increasing streaming penetration – streaming penetration is currently 15% globally today and is expected to increase to 25% (source: Goldman Sachs) over the next decade, driven by population growth and smartphone penetration growth. Increased streaming penetration increases the utility of the labels, thereby increasing pricing power.

Additional growth opportunities from the digital economy – music is a foundational element of high growth platforms such as social media, digital fitness and gaming. This expands the monetisation opportunity and benefits those players with the best and largest catalogue (where UMG is #1) whilst also increasing the value of that IP with new ways to consume it. These digital economy opportunities are currently 5% sales, and should grow at +10-15% p.a. adding ~+130 bps to sales growth. Key partners so far are below. Interestingly Epic Games actually created the virtual concert concept starting with Travis Scott in April 2020 which broke records and reached a global audience of 28 million people.

2. … driving EBITDA Margin expansion towards 30% by the end of the decade

UMG currently has an EBITDA margin of 21%, and I believe the following drivers should lead to expansion to 30% which is best in class.

Operating leverage – With improving monetisation being a core revenue driver, incremental drop through to margins is ~4%.

Positive mix shift from physical to streaming – The mix of digital/ physical sales within Recorded Music is currently 82%/18%, and I expect this to shift towards 95%/5% over the next decade. UMG generates 55% gross margin in streaming compared to 40% in physical as the cost of manufacturing, distribution, inventory and returns is removed.

Ongoing shift in consumption towards catalogue music - Catalogue royalties are more profitable given lower development and marketing costs. UMG has the largest and most valuable catalogue and is therefore the largest beneficiary.

3. AI is a significant opportunity, not a threat

AI is not a new phenomenon to the music industry. Over 20k AI-assisted tracks have already been uploaded daily to DSPs; despite this proliferation of content, UMG’s market share has stayed consistent.

AI lowers the barriers to entry for content creation, but raises the barriers to success. AI can boost productivity and creation capabilities but then it also creates a more crowded ecosystem which raises the bar for success. Therefore by definition, AI makes the role of the label more crucial for success.

The market is missing the potential for AI as a tailwind for UMG with proven examples:

UMG partners with Endel, to provide artists with AI to generate soundscapes and new versions of catalogue music.

UMG partners with HYBE (South Korean label) which uses AI to release tracks in multiple languages.

UMG is working on using AI to increase engagement between fans and artists.

I expect UMG to announce more AI-related partnerships over time.

The music industry is aligned at each part of the value chain to ensure controlled deployment of AI. There have been unsanctioned, non-original AI-generated songs that imitate well known artists which have achieved virality but the DSPs have promptly removed them to protect artists' rights - an example is the ‘Fake Drake’ track last year. Federal copyright laws and protections for artists will likely mitigate the risk further and even create compensation opportunities for artists and their labels. I believe that this time is different to when piracy posed an existential threat to the music industry beause of the labels’ leverage with the DSPs.

Key Risks

Disintermediation risk from DSPs – where DSPs can negotiate a lower royalty share with the labels as they grow larger.

However, the DSP model would not work without each of the 3 major labels’ content, whereas labels can survive without a DSP. Crucially the largest DSP, Spotify, stated on a recent earnings call that its relationship with the labels “has been the best it has ever been”, suggesting reduced risk of disintermediation.

AI is a threat – non-original content is created on social media where no royalty is paid to UMG.

However UMG controls 80% global copyrights and so has unmatched power to take punitive action.

A recent example is TikTok which has been a bad actor in terms of fees and the AI threat. TikTok was paying UMG just a LSD% of its advertising revenue for AI-generated music imitating UMG artists, versus the 20-30% that other DSPs pay. UMG accused TikTok of “trying to build a music based business without paying fair value for the music” (source: UMG Q4 2023 earnings call). UMG has stopped licensing music to TikTok, which likely accounts for ~80% of popular music! With TikTok only contributing to 1% of UMG’s total revenues, the downside is heavily skewed to TikTok rather than UMG so I expect a new, fairer deal will likely be negotiated.

Disintermediation risk from artists – where artists go direct-to-consumer.

Streaming has lowered barriers to entry for new artists, however it has also raised barriers to success. Labels have experience and industry connections that improve an artist’s chance of success materially such that breakthrough sans label is close to 0% probability.

High net content investment spend – UMG has invested increasing capital into net content which has raised market concern over FCF conversion.

A bear argument against UMG is the concern over a significant step up in cash payments for advances over the last 6 years.

An advance is a one off upfront payment to an artist which is recoupable against future royalties. For example UMG may agree to pay an artist $100m upfront in exchange for a multi album output agreement and the rights. UMG will only pay the artist a royalty once the advance has been recouped - i.e. an effective royalty holiday.

Payments have been as high as 8% of sales in 2020, but was 2% of sales in 2023. Bears assume the main driver of this significant content investment is artists' bargaining power increasing. UMG management have however clearly stated that the spike in 2020 was skewed towards superstar artists (Taylor Swift, Drake, The Weeknd, Justin Bieber) and that advances should normalise in the $150m level (1.5% sales) going forward. This to me is plausible; the number of superstars on the roster is finite so now that many have agreed new deals with UMG, these large upfront payments shouldn’t be repeated. Large payments to superstars have been incurred in return for expanded rights and extended time periods. The CFO has said “some of these deals are forever deals in terms of artist creativity and output...we'll have them for the rest of their careers" (source: Morgan Stanley conference 2021).

Overall I believe the large capital spend is misunderstood and should be associated with long term growth. UMG offers an attractive ROIC of 10-15% over the next 3 years.

Valuation

UMG currently trades at 20x 2024 EV/EBITDA which is undemanding given the structural growth trajectory, leading position in a global oligopoly, highly visible and resilient business model and low leverage.

UMG trades at an 8% premium to WMG. I believe the premium should be greater, to reflect UMG’s greater scale as #1 versus WMG at #3, higher comparative margins, lower financial leverage and superior corporate governance (WMG is controlled by Access Industries which holds 98% voting rights). An example of a stable industry where the best in class player trades at a premium to the #2 is Consumer Luxury, where LVMH trades at a +22% premium to Richemont.

UMG trades at a 25% discount to Netflix on EV/EBITDA, UMG’s equivalent leader in the Video Entertainment industry. This implies that the market is valuing “eyeballs” at a premium to “ears” despite that music is the most consumed form of entertainment globally at 20 hours a week (source: IFPI Report) v 12 hours on video. Arguably UMG should trade at a premium to NFLX given the superiority of the music industry to the video entertainment industry:

Content is more concentrated meaning a distributor needs content from all the majors, unlike in the Video industry where totality is not existentially necessary.

Distributors have limited exclusive/ proprietary content which favours the unit economics of the labels.

Music labels are less dependent on new “hits” given that catalogue makes up 60% revenues.

As an illustration, applying NFLX’s 27x EV/EBITDA multiple to UMG with a 10% premium would imply an IRR of 28% over 4 years.

Thanks for reading! As always please let me know your thoughts via the buttons below.